We hear talk of inflation constantly in financial news and economics textbooks, but rarely do we find the distinction made between price inflation and monetary inflation. Understanding this difference is key to understanding how our money works, and how the modern-day compares to many enlightening episodes throughout history.

Price inflation means a rise in price for goods and services – this is the inflation we are familiar with. When we talk about a McDonald’s hamburger steadily increasing in price over decades, we are talking about price inflation. Prices are denominated in units of money – like dollars or ounces of gold.

Monetary inflation means an increase in the supply of money. When a central bank like the Federal Reserve (‘Fed’) or European Central Bank (ECB) lower interest rates, do quantitative easing or otherwise ‘increase liquidity’, they are increasing the supply of money and causing monetary inflation.

Monetary inflation matters because it can cause price inflation. Price inflation occurs because money is a good with supply and demand, just like a hamburger. If the supply of money increases, the value of each unit of money decreases – which puts pressure on prices for all goods to rise.

History tells us that economies with high monetary inflation over long periods of time create oppressive societies with unequal wealth distributions that ultimately end in economic disaster. In this post, I’ll walk through how that happens.

Banking: How Banks Conduct Monetary Inflation

When the concept of banking first appeared in history, around the 7th century in China and the 15th century in Europe, gold and silver were the primary monetary instruments used in trade. Both gold and silver were well-suited to functioning as money because they are difficult to counterfeit, sufficiently rare (making each unit worth more) and easy to press into uniform shapes and sizes.

However, these metals were cumbersome and risky to transport, so entrepreneurs created the concept of a bank: a place that would store your gold and give you a slip, representing a claim on that gold. Eventually, trading partners started accepting these slips from reputable banks as payment, instead of physical gold. It’s likely that banks made their profits by charging customers for gold storage services. However, a new model was soon invented: lending.

When extending a loan, a bank essentially produced more claims on gold (slips of paper) than they had gold to back those claims. Then they charged an interest rate on the loan to earn a bit of profit. As long as borrowers repaid their loans and too many people didn’t come to claim their gold at the same time, the bank was solvent. The banker could now store gold at no cost, and even pay depositors a ‘yield’ on that gold as compensation for the risk that the bank might go bankrupt if enough borrowers didn’t repay their loans.

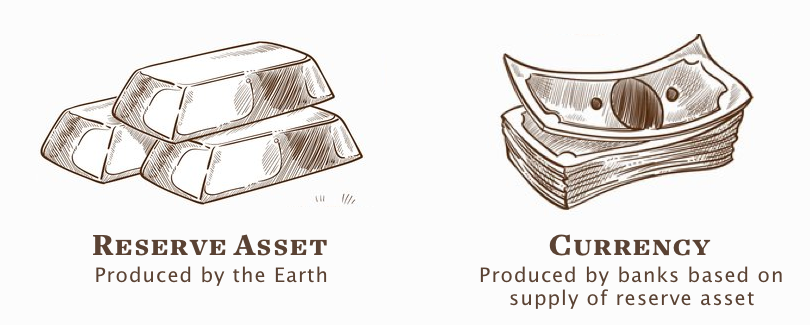

In this system, we can think of gold as a reserve asset and the slips of paper representing claims on gold as a currency. When banks extend loans by producing more claims on gold (paper slips) than they have the gold to pay back, they are creating currency. The banks were conducting monetary inflation on their own currencies.

When events caused a large number of borrowers to be unable to repay their loans, or a large number of currency holders to come asking for their gold, a deleveraging event would kick off. The bank might go bankrupt as it pays out all the gold it can to holders of its currency, and the currency supply would shrink back down until the currency in circulation matched the gold at the bank one-to-one.

In this world, monetary inflation was tied to the business cycle – the supply of currency expanded during good times and contracted during bad times. The supply of reserve assets, however, remained unaffected by these events. The laws of physics limited the amount of gold available in the Earth and made it difficult to find or produce otherwise.

Central Banking: Another Layer of Monetary Inflation

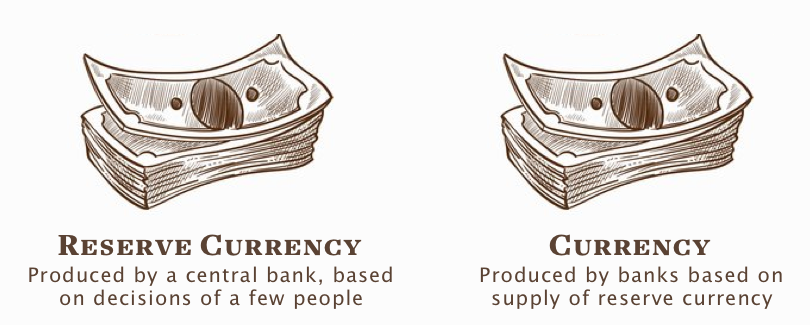

Central banks add a new layer to the previous example of a bank producing monetary inflation. Our global economy today is so dependent on several central banks and the world reserve currencies they control – like the dollar, Euro, and yen – that these currencies act like reserve assets.

When one of these central banks increases the supply of their currency, they are increasing the supply of the reserve asset. Commercial banks today, like Citi and JPMorgan, need to have a certain amount of reserve currencies on hand to make loans against, just like the bankers of ancient times needed gold. When commercial banks extend loans, they are creating more currency – claims on reserve currencies held at the commercial bank.

The labeling here is confusing, because we think of both the money in our bank account and cash in our hand as ‘currency’. However, if we want to compare today’s system to the days where banks held gold as a reserve asset, the cash in our hand is closer to a reserve asset while the money in our bank account is currency. We will call the cash in your hand a reserve currency and your bank account simply currency.

If we go back to our simpler model of an early bank, a central bank is like a gold producer – but instead of the laws of physics preventing the producer from creating more gold, there are no limits on the central banker producing more of their reserve currency.

This means central banks can act countercyclically – driving monetary inflation during bad times and reducing money supply during good times. They can attempt to centrally plan the market for reserve currency – the most important market in the world, because every business and consumer interacts with currency.

The stated goals of most central banks are to encourage full employment and stabilize prices. However, they often target a certain price inflation, like 2% per year, and attempt to change the reserve currency supply to achieve that rate of price inflation.

Measuring inflation is tricky – there are myriad places currency can go in an economy where it can affect prices. To get a read on price inflation, central banks primarily rely on a ‘price index’ – in the US, this price index is called ‘core inflation’ and it includes a select set of items the ‘average’ consumer purchases, without gas and food costs – which are deemed ‘too volatile’ to matter in the index, although they are crucial for everyday survival.

Central banks attempt to change the supply of reserve currency through several methods:

Interest Rate Manipulation

By buying and selling government debt for newly printed reserve currency, the central bank essentially makes it easier or harder for commercial banks to get their hands on reserve currency. With more reserves, these banks can take more risks and make more loans at lower interest rates to customers.

Quantitative Easing

Quantitative easing is a euphemism for “print a ton of reserve currency and put it in the banking system” – it is essentially a beefed-up version of the regular operations central banks conduct to control the interest rate and keep it at the central bank’s ‘target’ rate.

Helicopter Money

Helicopter money involves giving reserve currency directly to people by cooperating with the government to distribute stimulus checks. This is a last-ditch effort to restart spending and investment when the first two methods begin to fail.

The first two methods make for a great comparison to the origins of banking, where the risks commercial banks took were naturally limited by their ability to procure gold to back their loans and investments. Since today’s central banks produce the reserve currency that’s needed to back loans, commercial banks can take more and more risks if they expect the central bank to conduct a ‘bail out’ through interest rate manipulation and quantitative easing if the bank goes bankrupt.

So, when more reserve currency is put into the system, regular currency created by banks can expand exponentially. A small change in reserve currency can have a huge change in overall currency supply, if banks invest that money in loans and assets.

What impact does monetary inflation have on price inflation?

Monetary inflation and price inflation have a tight relationship in aggregate, but when looking at specific prices or price indices they can be quite tricky to connect.

Reserve currency is just like any other good – its value, and purchasing power, is dependent on its supply and demand. Increasing the supply of any reserve currency, then, puts downward pressure on the value of that currency. If commercial banks do as central banks hope, and expand the currency supply, prices naturally go up around the economy.

However, other simultaneous shifts can make this relationship harder to see. For instance, a recession or pandemic can cause a huge drop in consumer spending and rise in saving, which may counteract the monetary inflation done by a central bank and actually cause prices to drop in the short term. However, if the reserve currency injected into the system during a crisis is not quickly removed when the good times roll again, you can bet that price inflation will occur.

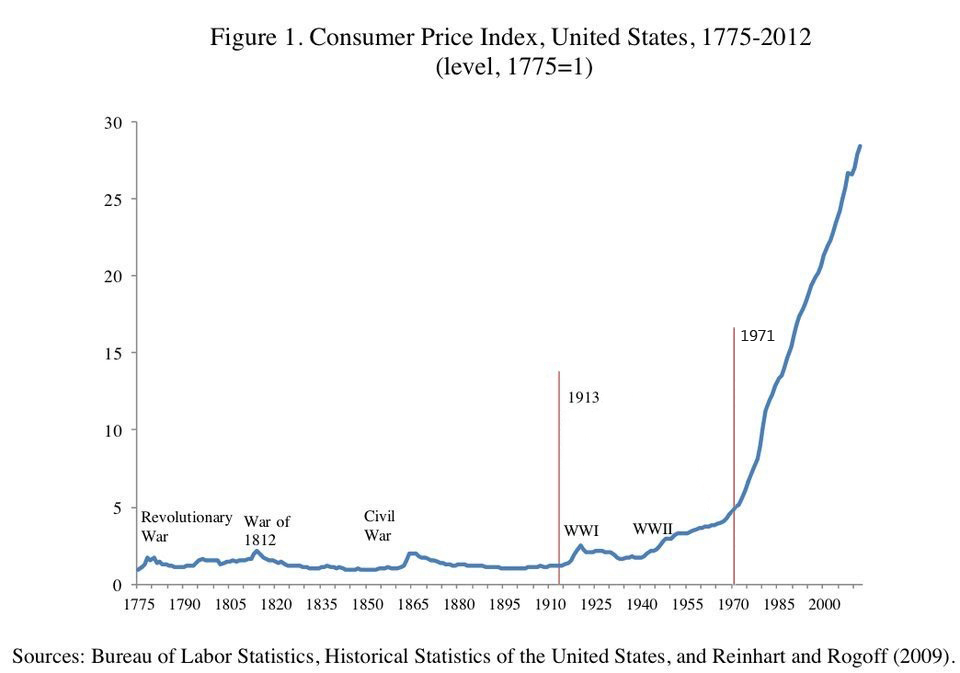

Without monetary inflation, we actually don’t see any significant price inflation over time. Just take a look at the US price index back through the 1800s – only wars, which were briefly financed through government deficit spending and increased currency supply, caused inflation. When the nation returned to a gold standard after these wars, prices returned to normal.

This is the ‘price stability’ many central banks claim to pursue – yet it only existed before the Federal Reserve, the US central bank, was created!

Who benefits from monetary inflation?

The central bank’s ability to produce reserve currency gives it a lot of power to decide winners and losers in the markets. Because monetary inflation can cause price inflation, central banks and commercial banks can end up enriching some at the expense of others.

How can price inflation enrich people?

Through the Cantillon Effect. Pointed out by a French economist in the 1700s, the Cantillon Effect describes how the first entities to receive newly created reserve currency benefit the most, with the last entities benefitting the least – or actually being harmed by rising prices.

Price and monetary inflation can benefit the rich and hurt others when new currency ends up being used by banks and the wealthy to buy financial products like stocks and bonds. This causes massive rallies in investment products, which make up a large share of capital for the wealthy and progressively smaller shares for poorer classes. Plust, these products are not included in ‘core inflation’, so the central bank can continue to enrich the wealthy and powerful without increasing the ‘inflation’ we see talked about on the news.

What are some historical examples of monetary inflation?

Monetary inflation dates back to the dawn of civilization. Unfortunately, we find that the fall of societies often coincides with monetary inflation.

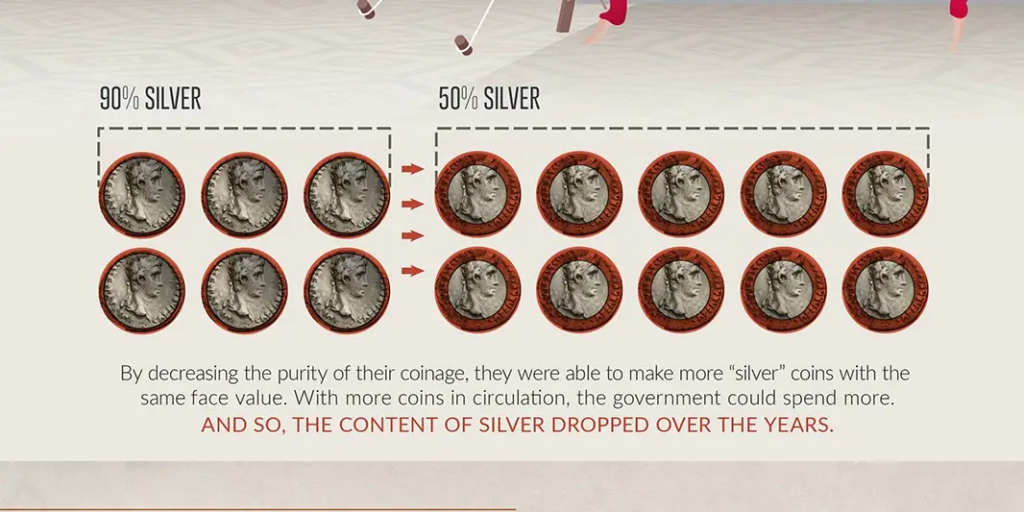

The Roman empire is a great example, with the Pax Romana ending around the time monetary inflation began in earnest. Several centuries later, the Roman empire was in shambles, and the Medieval Dark Ages began. The St. Louis Federal Reserve, ironically, understands this well and created a lesson plan around Roman currency debasement. In the lesson, they detail how the Roman government debased Roman coinage by mixing tin into silver coins, benefitting the spending power of the government, which were the first to spend the ‘new currency’ produced by debasement.

Germany following the first World War is another example of monetary inflation. Saddled with huge reparations payments to the victors, Germany struggled to keep its economy afloat. In order to buy more gold to pay reparations with, the German central bank produced a massive amount of German Marks, ultimately destroying the purchasing power of their currency and the wealth of their nation. Destitute economic conditions drove Germans to increasingly radical political positions, ultimately causing the rise of one of the most ruthless, despotic and horrifying regimes in history.

Other examples include Zimbabwe, Argentina, and Venezuela. All begin with some trigger caused by a government – whether that be heavy government debt levels, wealth redistribution programs or simple greed and corruption – but end in economic instability and destitution for the large majority of people.

Is monetary inflation happening today?

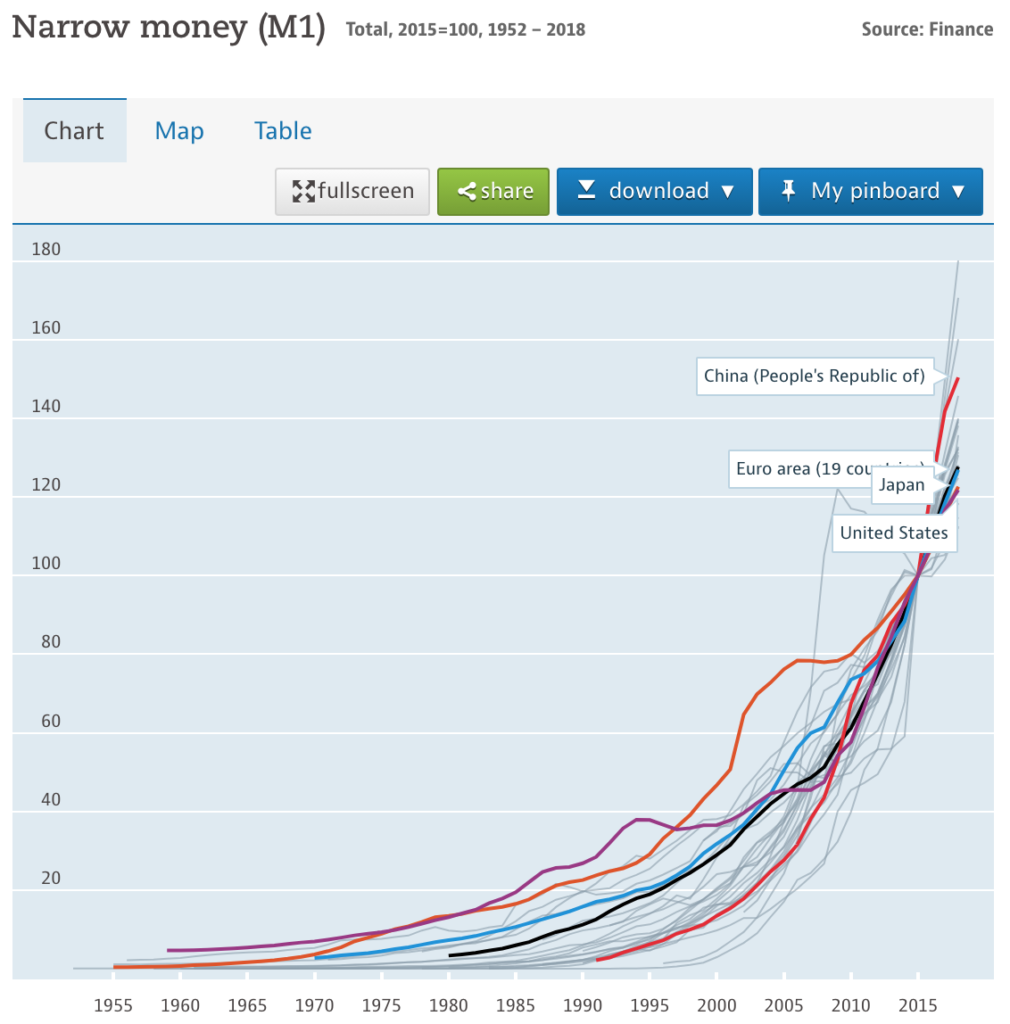

Today, we thankfully have a lot of freely accessible data from central banks to understand whether they are producing more of their reserve currencies and conducting monetary inflation.

Let’s look at the supply of a few of the most important currencies in the world – the dollar, euro, yen, and Chinese Renminbi. The metric we will look at is the supply of the reserve currency, not all the circulating units of these currencies in existence – which is much harder to measure.

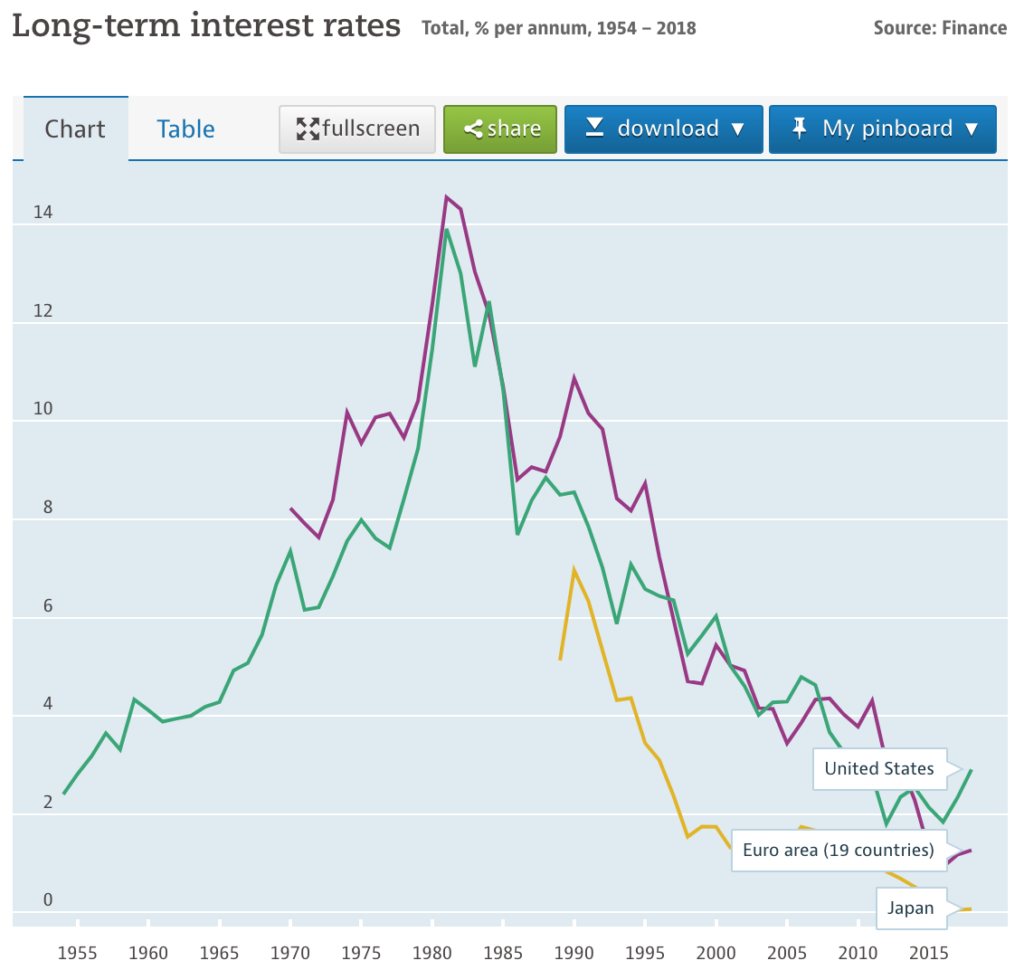

Key interest rates in major economies can also give us a sense for how much currency is being produced in an economy: interest rates that are trending up mean currency supply is likely shrinking, while interest rates trending down mean monetary inflation is likely occurring.

Unfortunately, instead of monetary inflation being isolated to one country as it has in many examples in recent history, it is now systemic. All economies may be pulled down by the eventual demise of this system, instead of just one part of the globe.

What can be done about this?

A return to a world where the money supply is regulated by the supply of a reserve asset that nobody can produce more of, instead of a reserve currency that central banks can print more of at will. This would mean governments returning to a sound money standard, like a gold standard. As a highly interconnected global economy, we are far from the days of using gold as a global reserve asset, though gold’s price in terms of reserve currencies has certainly increased since the end of the gold standard in 1971. Governments also seem unlikely to make this tough choice – preferring to attempt to ‘print their way out of trouble’ as they have so many times through history.

It will be up to each individual to choose to hold the money they believe should run the economy – whether that be gold or a sound money with the ability to move around the globe in an instant – Bitcoin. Through each individual’s free choice of the best money, the world’s inhabitants can avoid disaster at the hands of monetary inflation.

If you like my work, please share it with your friends and family. My goal is to provide everyone a window into economics and how it affects their lives.

Subscribe to email updates when new posts are published.

All content on WhatIsMoney.info is published in accordance with our Editorial Policy.